How Factoring Companies Secure Receivables, and Why You Still Need to Protect Yourself

If you are a contractor or supplier who is regularly involved in construction projects, you may have considered doing business with a factoring company to help even out your cash flow. As you probably know, factors purchase your outstanding invoices at a discount, advance you part of what you are owed, and then collect from the contractor or owner you are working for. The terms vary, but typically you can get 80 to 90 percent of the value of the outstanding invoices up front. If the factor can collect all of the invoice amounts due, it usually charges a factoring fee that is a percentage of the total. Any remaining balance over what you have already received is then transferred to you.

Factoring Does Not Remove Your Risk

The factor usually will not assume all of the risk of collecting unpaid invoice amounts. Ultimately, you remain responsible for collection efforts if the owner or contractor does not pay. That can mean owing the factoring company for advances you have already received if payments are late or never collected. In addition, much like a loan, the longer it takes the factor to collect on the invoices it purchases, the higher the fees it charges.

How Factors Secure What They Advance

Factors typically file a UCC financing statement against the invoices they purchase from you. That means if you have already pledged your accounts receivable, for example as collateral for a line of credit or a short-term loan, you may have difficulty factoring invoices that are already pledged. It can take some effort and discussion with existing lenders to separate the invoices the factor is purchasing from other accounts receivable that may already be pledged.

What many factors will not do is fully step into your shoes and take on all of the collection risk for the invoices they purchase. Those who provide this kind of non-recourse financing charge more, because the factoring company assumes the payment risk. That is why it is so important, even if you regularly use factors and have had good results in the past, to be in a position to protect yourself if it turns out the factor cannot collect all or part of what you are owed.

Protecting Your Factored Receivables

Protecting your ability to collect from owners and contractors comes down to two things: having a system in place, and actually using it. A project data sheet for each new job can help you gather the information you need to properly secure your right to get paid. Project data sheets compile a wide range of information about each project, much of which you probably already have in one place or another. Putting it in a single document helps you take the proper steps at the proper time to secure your receivables.

Using Your Compliance System

Once the information is gathered, the next step is to use it effectively. The requirements for mechanics liens and other forms of payment security vary considerably from one state to another and from one project type to another. Knowing the particular requirements for your project, and meeting them, is what turns a compliance system into actual protection.

Whether or not you are exploring working with a factoring company, the steps you take to protect your receivables are what get you paid, from preliminary notice and lien filing to collecting on a payment bond or negotiating with a slow-paying owner or contractor. Contact us to set up a consultation and learn more about how we can help you get paid.

Related Articles

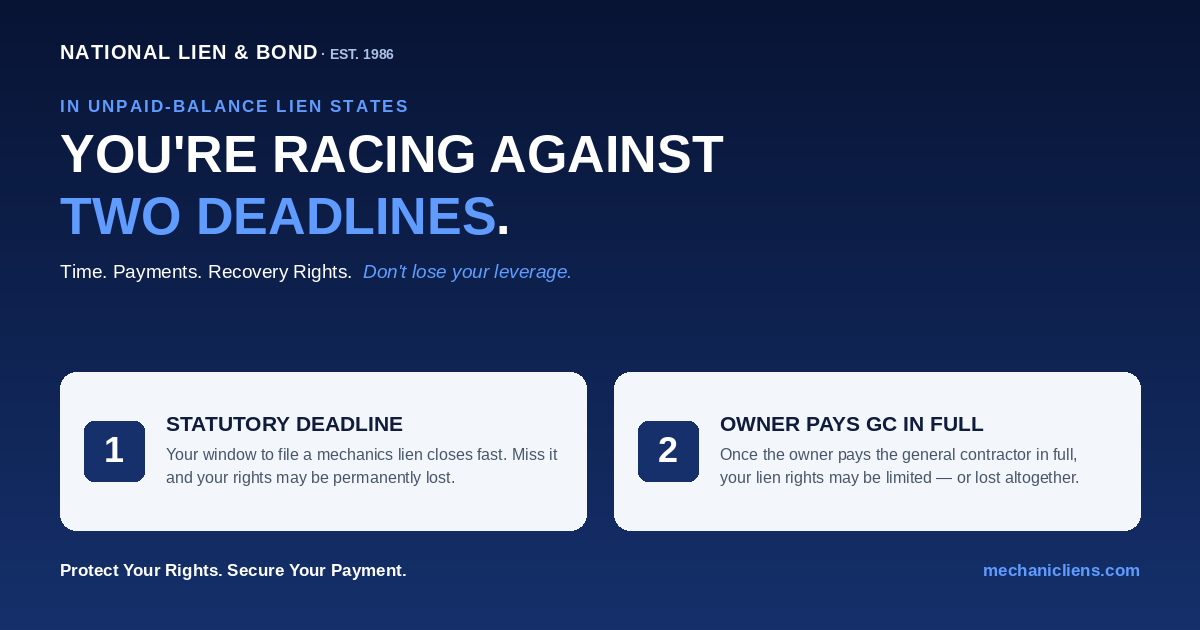

Unpaid-Balance Lien States: Why You're Racing Against Two Deadlines, Not One

In an unpaid-balance lien state, the calendar deadline to record your lien is only half the race. The hidden second deadline is the moment the owner finishes paying the general contractor - because that payment can shrink or erase the fund your lien attaches to. This guide explains both deadlines, why subcontractors and suppliers lose money even when they file 'on time,' and the notice-and-timing strategy that protects your leverage.

Read Article

Connecticut Mechanics Lien Law: Notices, Deadlines, Lien Rights, and Contractor Registration

Connecticut treats original contractors and lower-tier claimants differently. This guide covers the lower-tier notice of intent, the 90-day certificate recording deadline, the 30-day owner-service requirement, the one-year foreclosure-and-lis-pendens deadline, the lienable-fund limit on subcontractor liens, who can claim, and how Home Improvement Act and New Home Construction registration affect enforcement.

Read Article

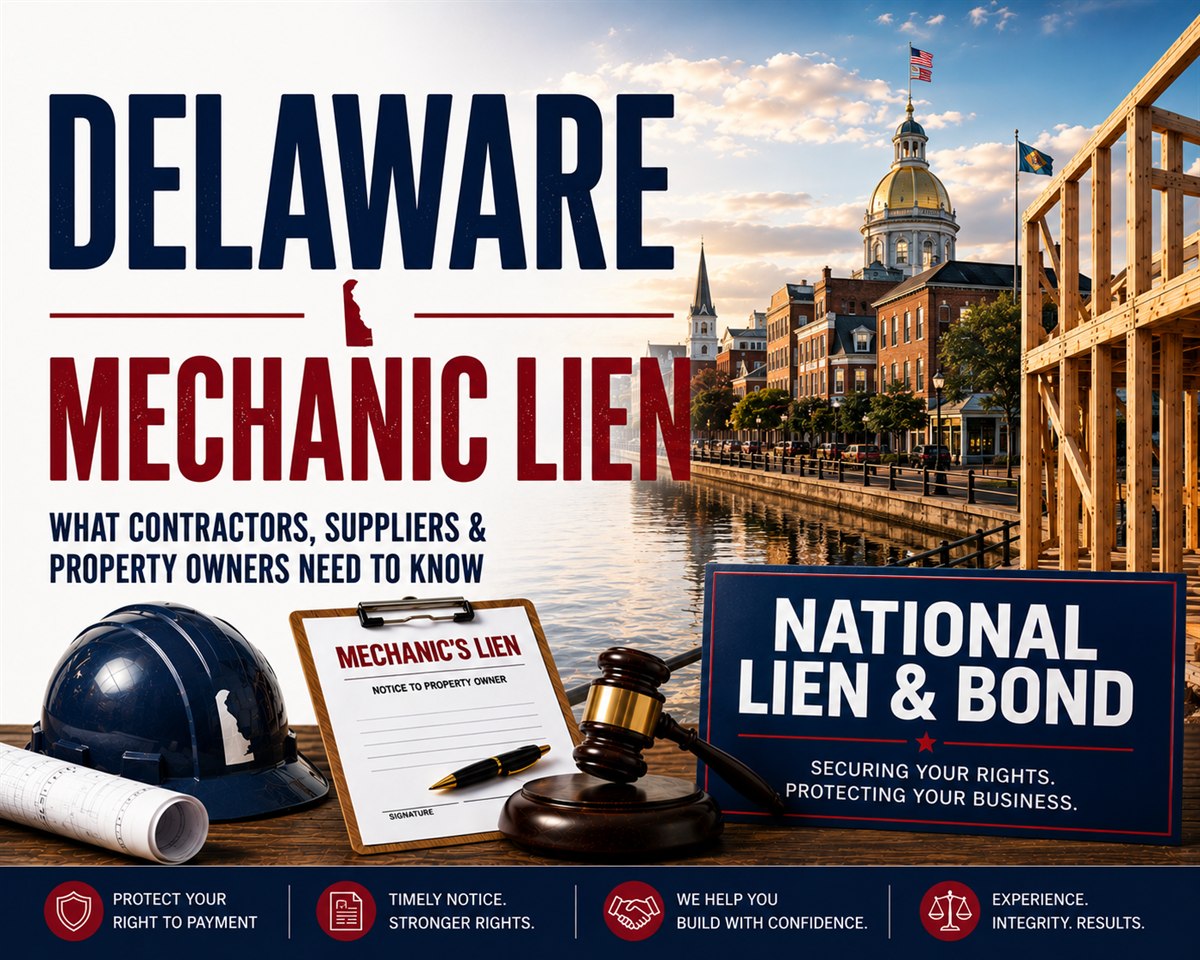

Delaware Mechanics Lien Law: Statement of Claim, Deadlines, Lien Rights, and Contractor Registration

Delaware enforces mechanics liens through a strictly construed statement of claim filed in Superior Court. This guide covers the 180-day and 120-day filing deadlines, the prior-written-consent rule for tenant work, the statement-of-claim pleading elements, the $25 threshold, who can claim, and Delaware contractor registration and business licensing.

Read Article