What is a Surety Bond and How Can it Help Ensure Prompt Payment on Your Project?

Even those who have worked in the construction industry for years might not know everything there is about the different types of documents used to ensure payment. So if you find yourself asking, "what is a surety bond?" then you aren't alone.

Like private property owners, cities, states and federal agencies own real estate. When they acquire the land a deed is recorded for both public and private owner. When working on a public or federal project you can still be protected by a payment bond claim, and in many states a lien on public funds is sometimes available.

When owners want to ensure that there are no liens they require the general contractor (GC) to furnish a surety bond. A bond is typically required on most public construction projects from the federal level all the way down to local municipal projects.

What is a Surety Bond?

One option owners have in this situation is to require the GC to issue a surety bond. A surety bond is essentially a pile of money or resources, generally provided by an insurance company or a financial institution, that is set aside to serve as security on a project. In the event an owed payment isn't made, you can then make a claim against the resources set aside as the surety.

Knowing the cash is there and available if needed helps facilitate cash flow throughout the entire project. If the project does run into a problem, laborers are able to make a claim against the surety as their compensation. In many states, there is a statutory requirement that public construction projects use surety bonds, though they are used on private construction projects as well.

Payment Bonds and Performance Bonds

The most common types of surety bonds used on construction projects are payment bonds and performance bonds. Payment bonds are issued by the general contractor to the subcontractors and suppliers and ensures payment is made down the chain to all parties on the project. If the general contractor does not make a payment it should, or cannot due to bankruptcy, then the payment bond protects the rest of the companies involved in the project.

A performance bond, meanwhile, is designed to protect the owner of the project from loss in the event the project is not completed. In essence, it provides financial assurance that the project will be completed to certain specifications for a certain amount. If the general contractor then does not meet the terms of the agreement, the owner can submit a claim against the performance bond to complete the work.

In many cases, surety bonds consist both of performance bonds and payment bonds, protecting the owner of the property and project against many different possibilities of project failure. For federal projects, a performance bond must be posted by the general contractor any time the value of the project exceeds $100,000.

Bond Claims

Making a bond claim involves submitting the appropriate paperwork to the surety bond holder and following their instructions. Be sure to ask the GC on both public and private jobs for a copy of their payment bond before starting work. If you need help understanding the contractual requirements of the bond, how state and federal laws may apply, or what you should do, reach out to the team at National Lien & Bond. We can help you understand your specific situation and monitor and streamline the bond and mechanics lien process across all your projects in every state. For more information on how you can protect yourself click below for a free consultation.

Related Articles

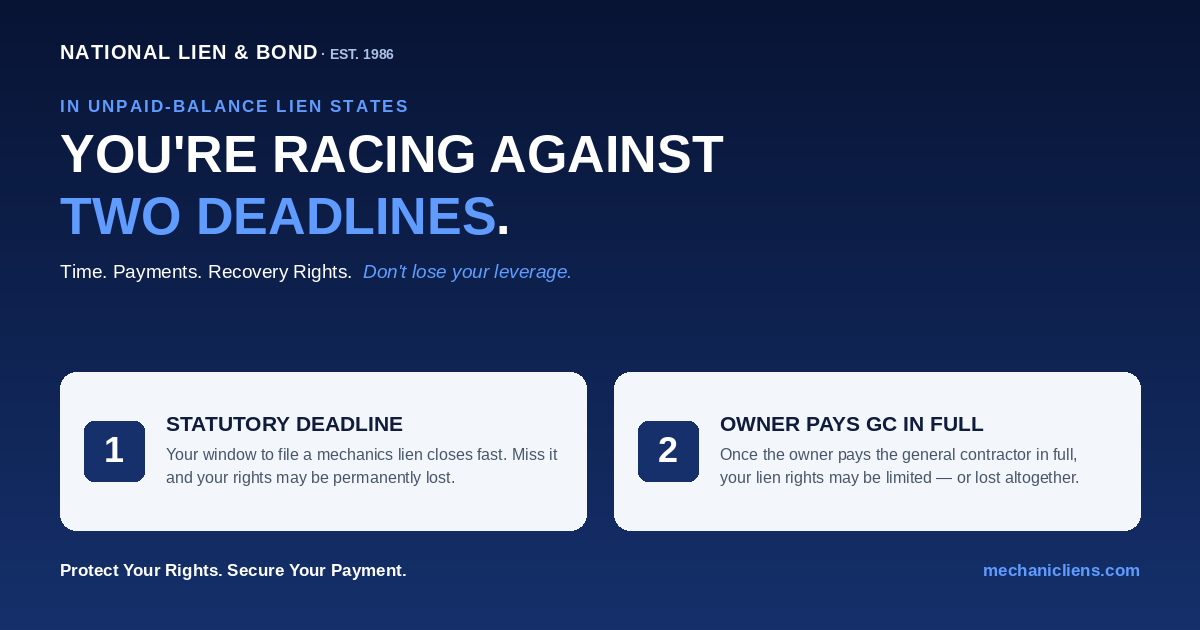

Unpaid-Balance Lien States: Why You're Racing Against Two Deadlines, Not One

In an unpaid-balance lien state, the calendar deadline to record your lien is only half the race. The hidden second deadline is the moment the owner finishes paying the general contractor - because that payment can shrink or erase the fund your lien attaches to. This guide explains both deadlines, why subcontractors and suppliers lose money even when they file 'on time,' and the notice-and-timing strategy that protects your leverage.

Read Article

Connecticut Mechanics Lien Law: Notices, Deadlines, Lien Rights, and Contractor Registration

Connecticut treats original contractors and lower-tier claimants differently. This guide covers the lower-tier notice of intent, the 90-day certificate recording deadline, the 30-day owner-service requirement, the one-year foreclosure-and-lis-pendens deadline, the lienable-fund limit on subcontractor liens, who can claim, and how Home Improvement Act and New Home Construction registration affect enforcement.

Read Article

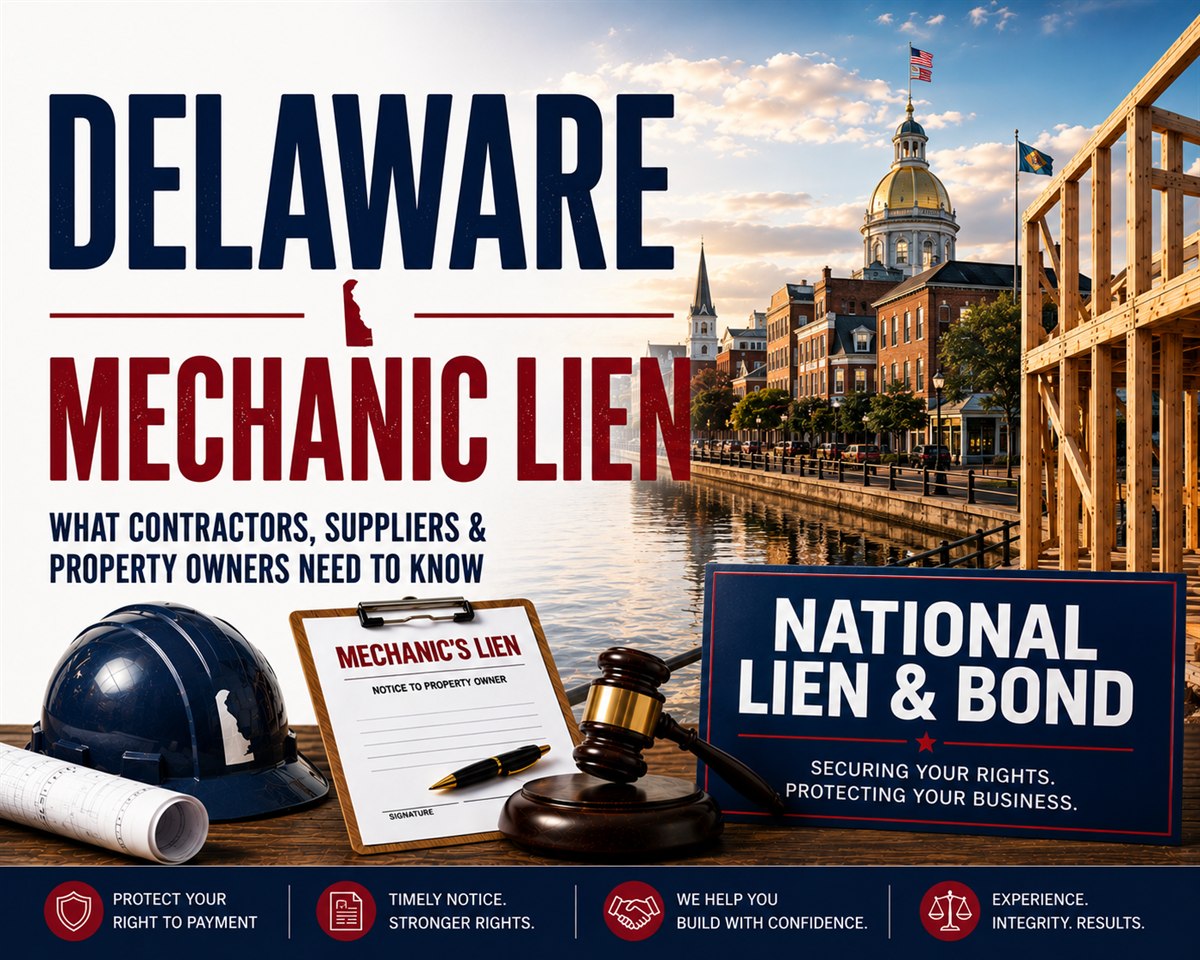

Delaware Mechanics Lien Law: Statement of Claim, Deadlines, Lien Rights, and Contractor Registration

Delaware enforces mechanics liens through a strictly construed statement of claim filed in Superior Court. This guide covers the 180-day and 120-day filing deadlines, the prior-written-consent rule for tenant work, the statement-of-claim pleading elements, the $25 threshold, who can claim, and Delaware contractor registration and business licensing.

Read Article