Performance Bonds - The Ins, Outs, and How They Affect You on a Public Construction Project

When it comes to schedules and timelines for construction projects, those with experience will agree there are too many possibilities of curve balls that just cannot be accounted for. However, if theres one thing all players involved expect, it's to get paid. For large scale commercial jobs, Surety bonds provide you with the assurance of getting paid.

There are generally two types of relevant bonds: payment bonds and performance bonds.

Performance bonds are used by the project owner to file a claim against the payment bond if needed. This serves as assurance that the general contractor will complete the contract on time. If the subcontractors and the material suppliers don't get paid, they can file a claim against the payment. While you can't file a mechanics lien on a public project, you can file a bond claim and in many states a lien on public funds.

Performance Bond Details

A performance bond is a surety that binds the general contractor and the governmental entity (which owns the project) to the project's details and its timely completion. The performance bond ensures that the contractor performs as specified in the construction contract. If the contractor fails to do so, the project owner can submit a claim against the bond. In the end, the bond holder (often an arm of an insurance company that specializes in construction bonds) assumes responsibility for seeing the project to completion or alternatively, can payout the value of the bond.

Requirements vary between federal, state, and local governments. The surety company can be involved and tasked to pressure both sides towards completion. The surety company has a vested interest in ensuring the work is performed to specifications, and that the subcontractors and suppliers are paid on time.

How Performance Bonds Benefit Contractors

The cost of a performance bonds vary, but generally represent a fraction of the value of the contract. If a performance bond is required, it can generally and easily be obtained by working with a surety company. Once a company's bid has been selected, that company obtains bonds. Generally, you obtain both a performance and a payment bond at the same time so that both sides of a particular transaction, as well as all subcontractors and suppliers involved, are protected in the event of a problem.

While the obvious benefits of performance bonds might be for the owner of the project, they also protect subcontractors and ensure work carries on regardless of any issues the general contractor may encounter. Knowing that a third party protects the work and keeps it on schedule ensures a cash flow to those further down the contracting line.

If you'd like to learn more about construction bonds, or you're in need for specialized advice, reach out to the National Lien and Bond team. With dedicated expertise in the construction industry all over the USA, our team can quickly address and respond to your concerns. In addition, they offer the industry's most highly informative lien seminars to ensure your entire management team is up-to-date about mechanics liens and construction bonds.

Related Articles

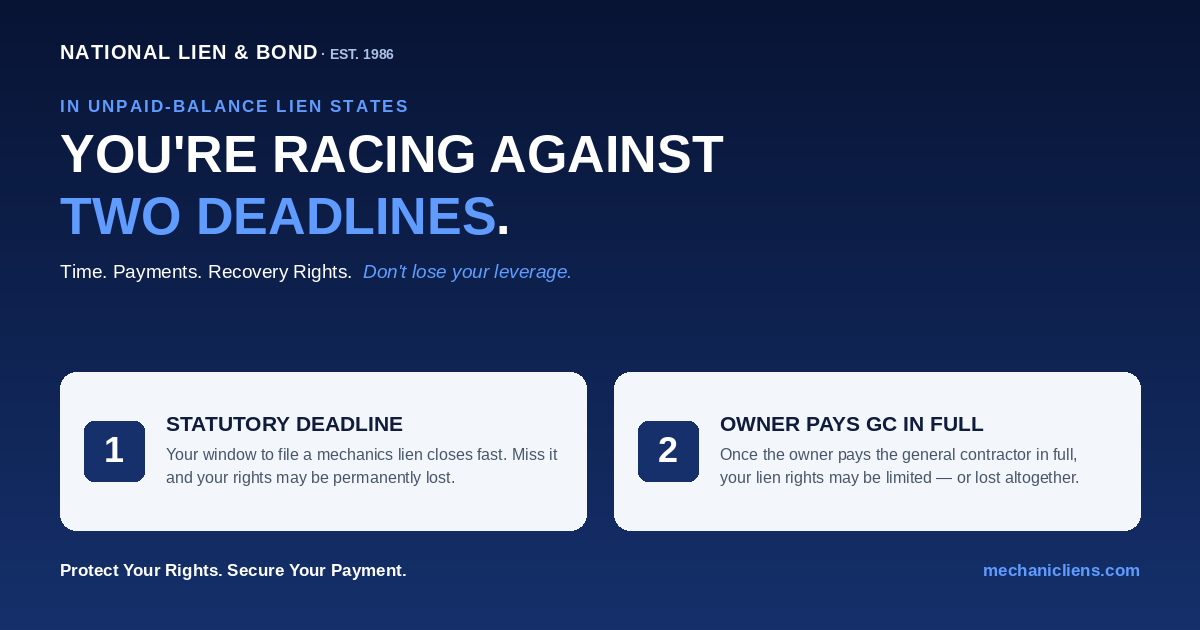

Unpaid-Balance Lien States: Why You're Racing Against Two Deadlines, Not One

In an unpaid-balance lien state, the calendar deadline to record your lien is only half the race. The hidden second deadline is the moment the owner finishes paying the general contractor - because that payment can shrink or erase the fund your lien attaches to. This guide explains both deadlines, why subcontractors and suppliers lose money even when they file 'on time,' and the notice-and-timing strategy that protects your leverage.

Read Article

Connecticut Mechanics Lien Law: Notices, Deadlines, Lien Rights, and Contractor Registration

Connecticut treats original contractors and lower-tier claimants differently. This guide covers the lower-tier notice of intent, the 90-day certificate recording deadline, the 30-day owner-service requirement, the one-year foreclosure-and-lis-pendens deadline, the lienable-fund limit on subcontractor liens, who can claim, and how Home Improvement Act and New Home Construction registration affect enforcement.

Read Article

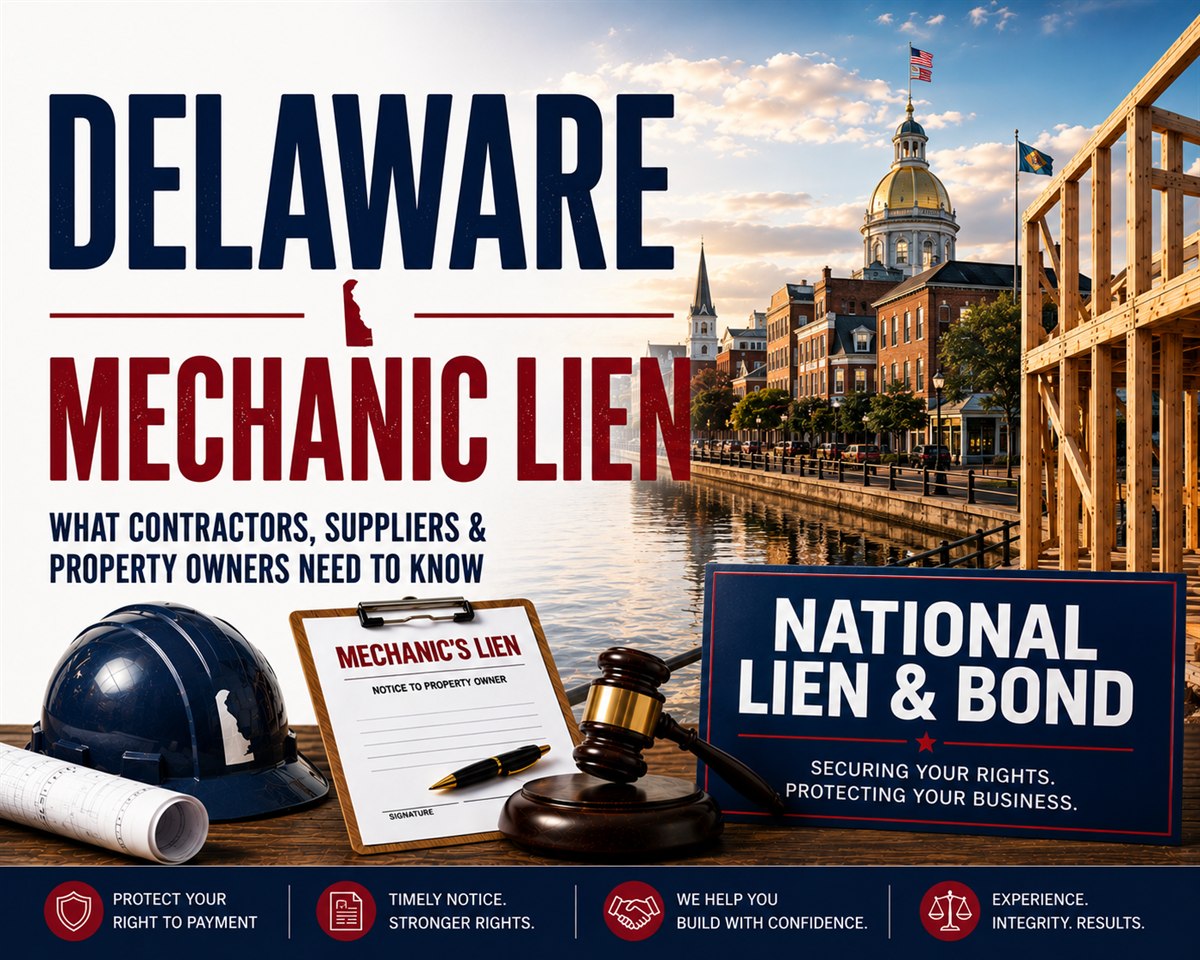

Delaware Mechanics Lien Law: Statement of Claim, Deadlines, Lien Rights, and Contractor Registration

Delaware enforces mechanics liens through a strictly construed statement of claim filed in Superior Court. This guide covers the 180-day and 120-day filing deadlines, the prior-written-consent rule for tenant work, the statement-of-claim pleading elements, the $25 threshold, who can claim, and Delaware contractor registration and business licensing.

Read Article